Across WhatsApp, Email, SMS/RCS, and Apps, financial services brands have built a multi-channel reach; what most haven’t built is the architecture to carry the journey through

There is a number that sits quietly in every banking and financial services marketing review, one row below the metrics that get celebrated.

- Open rates above 90%

- Click-throughs at 45-60%

- Segments sharp enough to drive >50% sales

- Creatives clocking millions of impressions

And then, at the bottom of the deck, the conversion number. It rarely matches the intent the campaign generated.

The room recalibrates quickly. Someone says the landing page needs work. Someone else schedules a retargeting review. The conversation moves on.

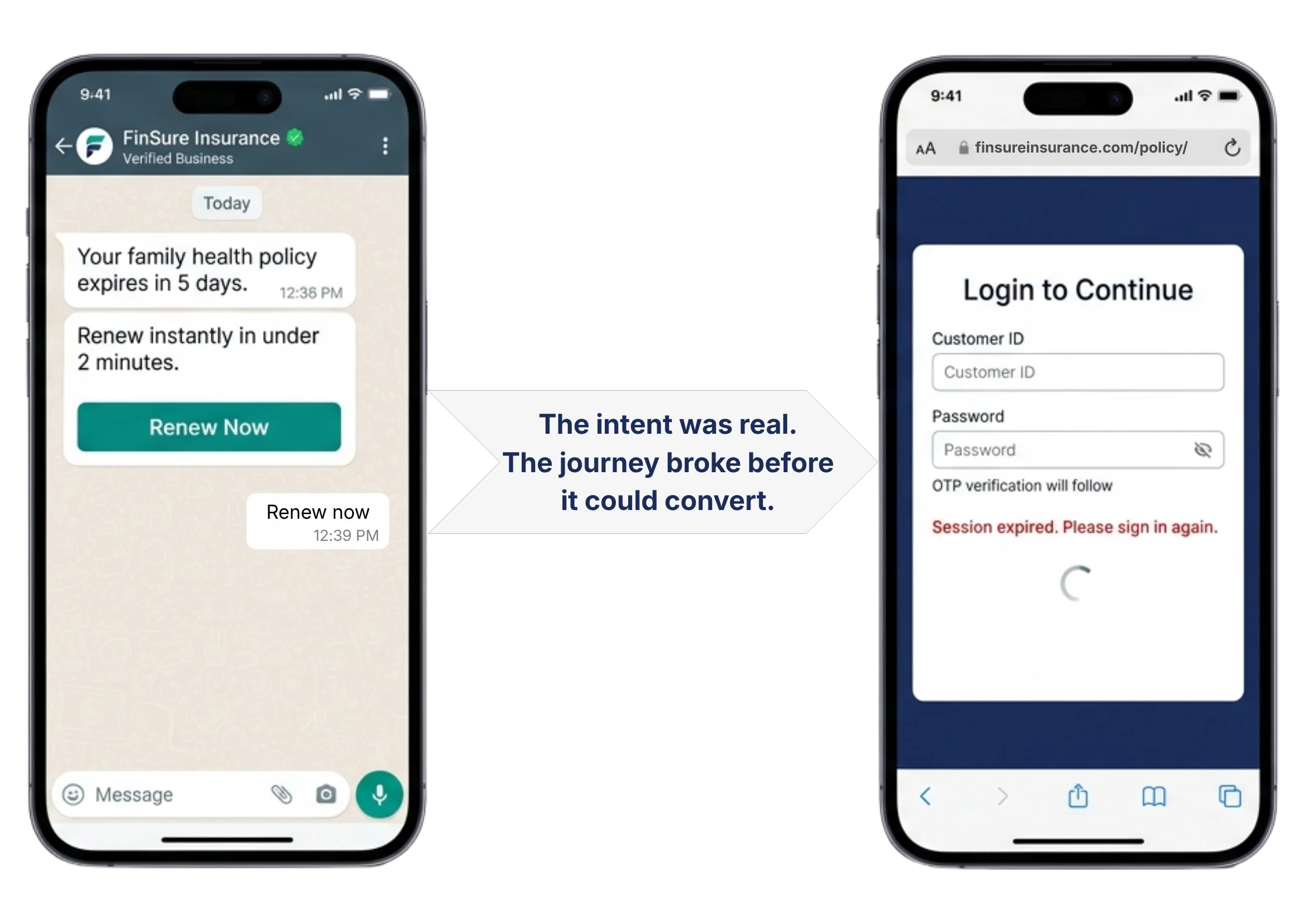

What rarely gets named is the harsh reality. The customer opened the message. They clicked. And then the journey asked them to start over, on a different channel, with no memory of what brought them there; no context, no journey state, no continuity. By the time they reached the transaction screen, a measurable share of them had already left.

In 2025, inconsistent omnichannel experiences drove a 7.5% churn rate among Gen Z banking users alone, the very cohort every financial services brand is spending most aggressively to acquire. Omnichannel banking clients, by contrast, deliver a customer lifetime value 42% higher than single-channel customers. And in Southeast Asia, where the battle for digital wallet primacy is sharpest, acquiring a new BFSI customer now costs five times more than reactivating an existing one.

The gap between those numbers signifies journey continuity, and that is the handoff trap. And in 2026, across India and Southeast Asia, it is the most expensive inefficiency that BFSI marketing budgets are carrying without a line item.

What the Handoff Trap Actually Is

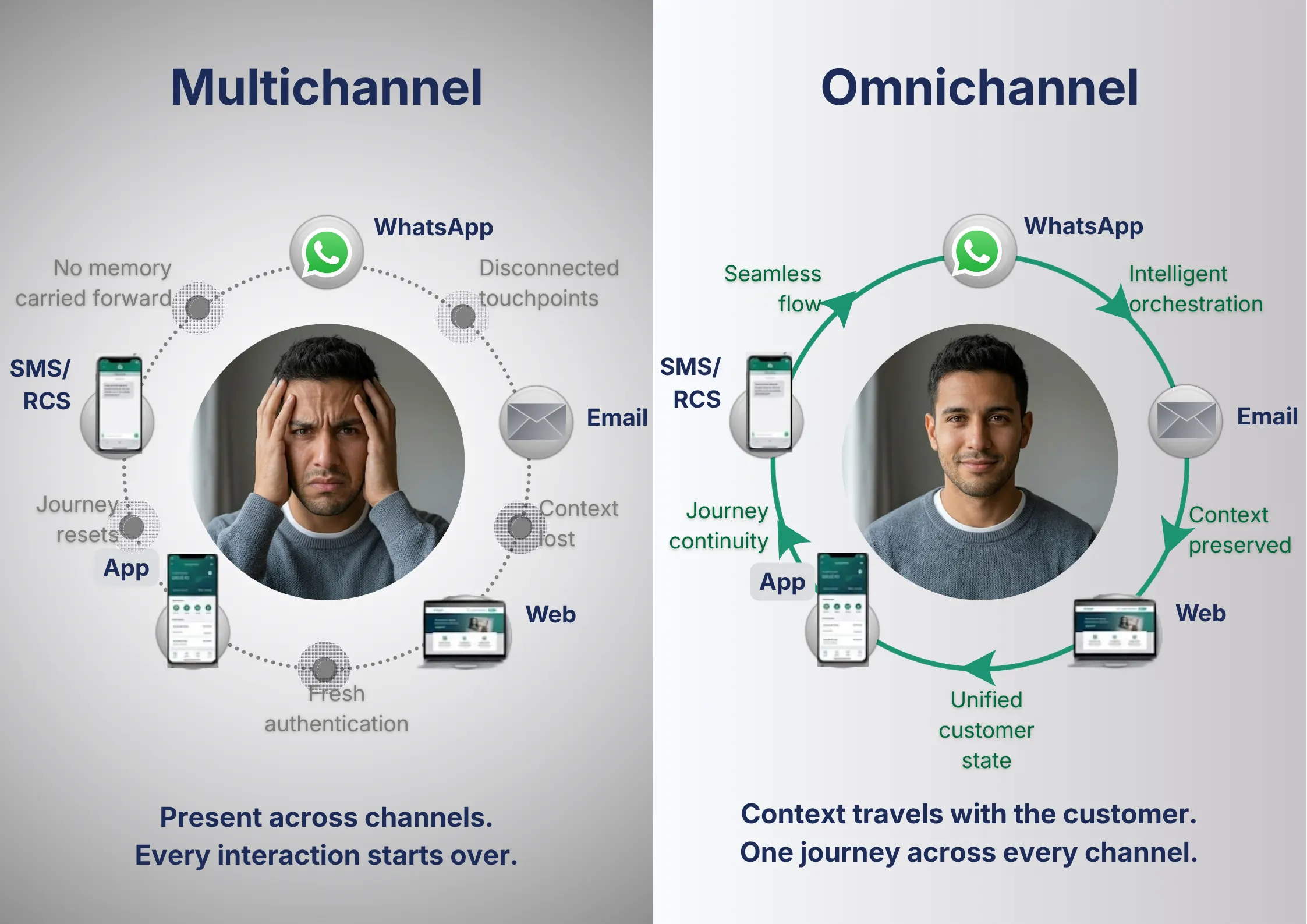

The handoff trap is not about any single channel underperforming. It is about what happens in the space between channels: the moment a customer’s intent, formed on one channel, is asked to survive a transfer to another with no context carried forward.

In most BFSI engagement stacks today, that space is not designed. It is the accumulated result of vendor decisions made at different points in time: a WhatsApp BSP selected for broadcast reach, a CPaaS layer added for authentication, an app built on a different timeline, and a payment gateway integrated last. Each piece was chosen for what it does in isolation. None of them were designed to hand off the customer seamlessly to the next.This is also where the omnichannel illusion lives. Most financial services brands believe they are already omnichannel; present on WhatsApp, Email, their app, and beyond, running coordinated campaigns with a CDP underneath. But omnichannel presence is not omnichannel continuity.

A brand can be present on five channels and still lose the customer’s context every time they move between them. Latest McKinsey research shows more than 50% of customers engage with 3 to 5 channels during a single purchase journey, not by choice but because the architecture demands it. Each move is a moment where context can be lost. In financial services, it almost always is.

The result is a journey that looks unified in a campaign brief but arrives broken in a customer’s hands.

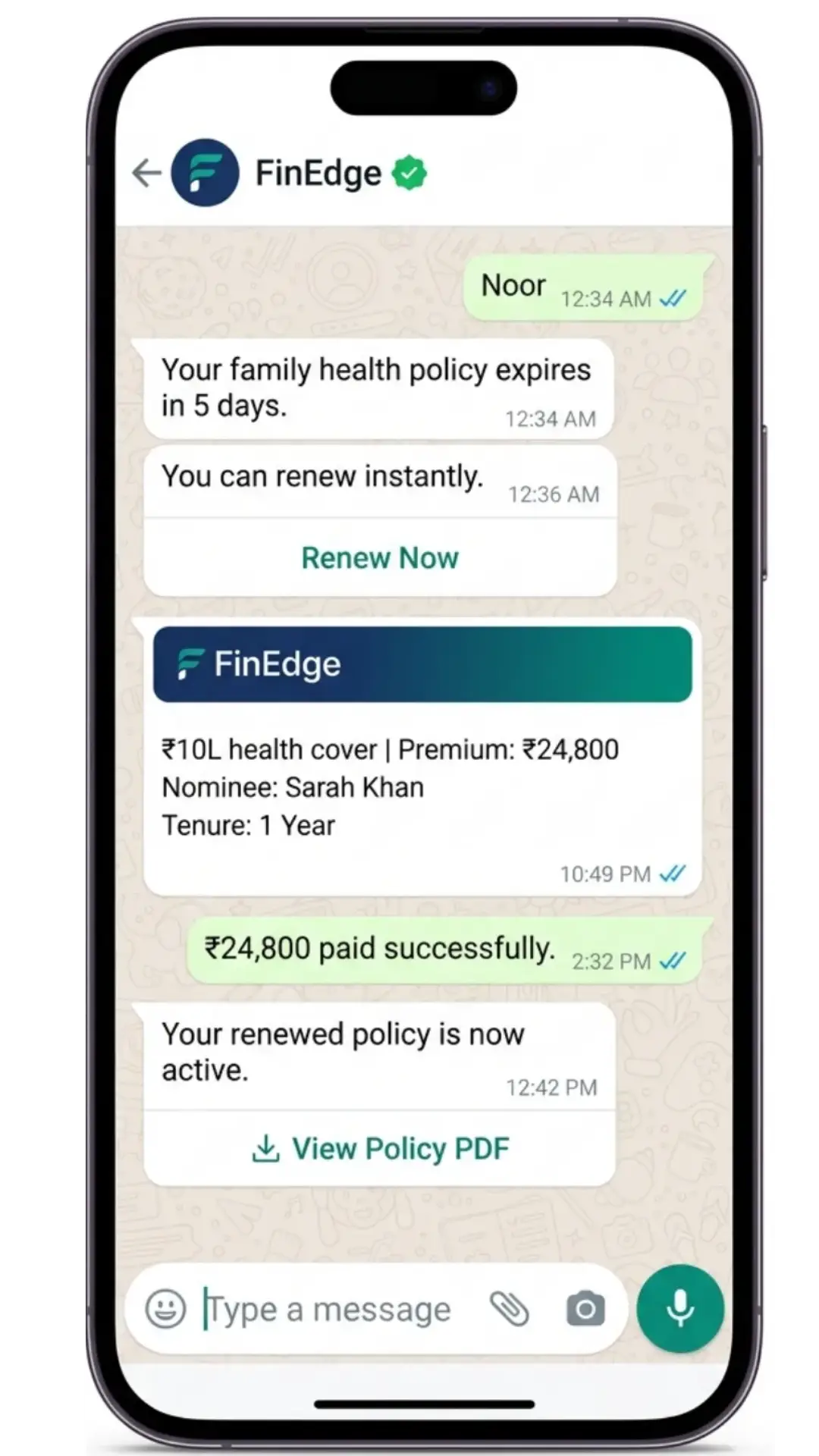

- A policyholder receives a renewal nudge on WhatsApp, clicks through, and lands on a browser-based portal that doesn’t know they came from a renewal reminder, asking for a Customer ID as if meeting them for the first time.

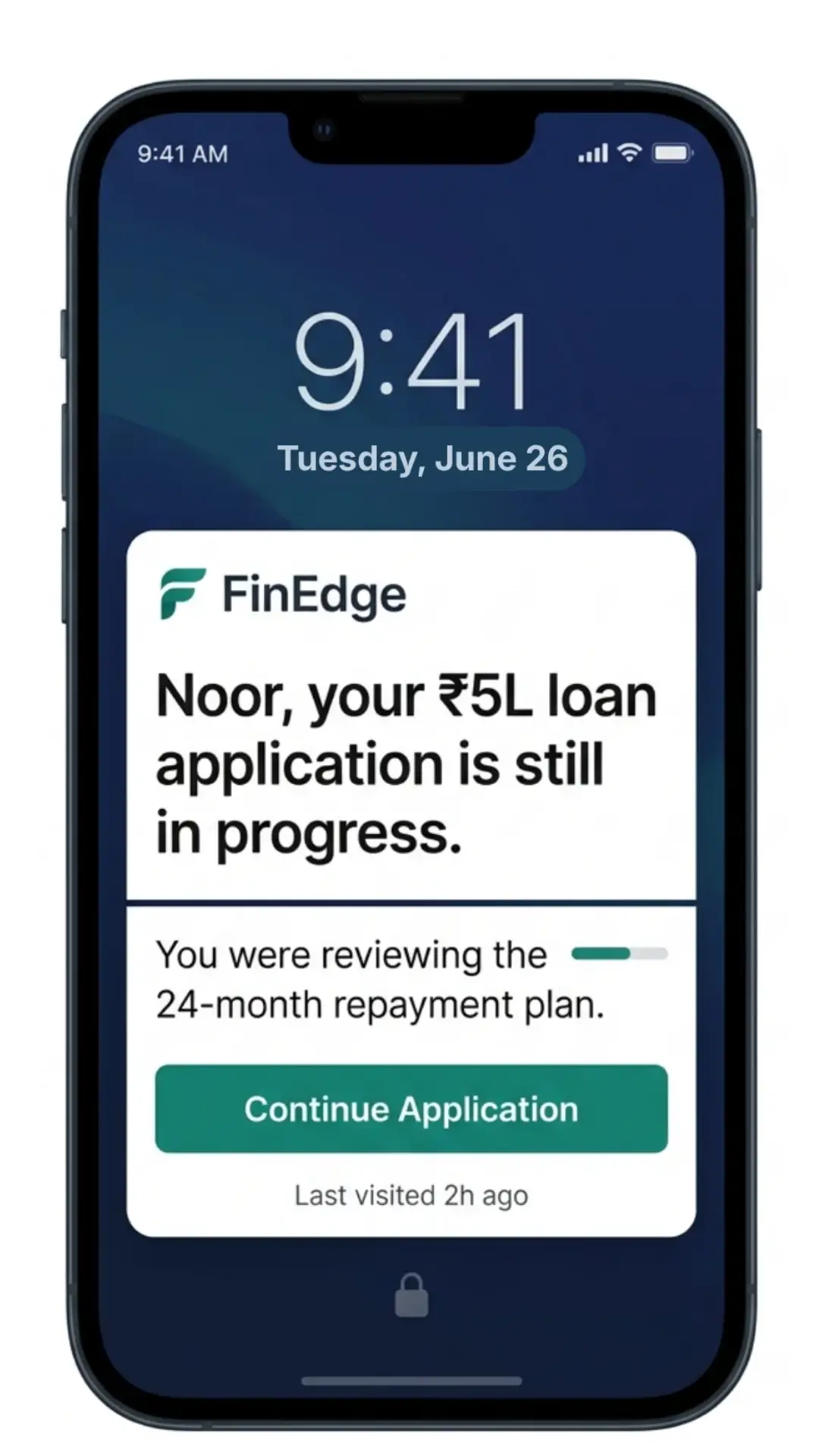

- A pre-approved loan offer surfaces inside a banking app, but the next screen re-collects information the bank already holds, treating a known customer like a cold applicant.

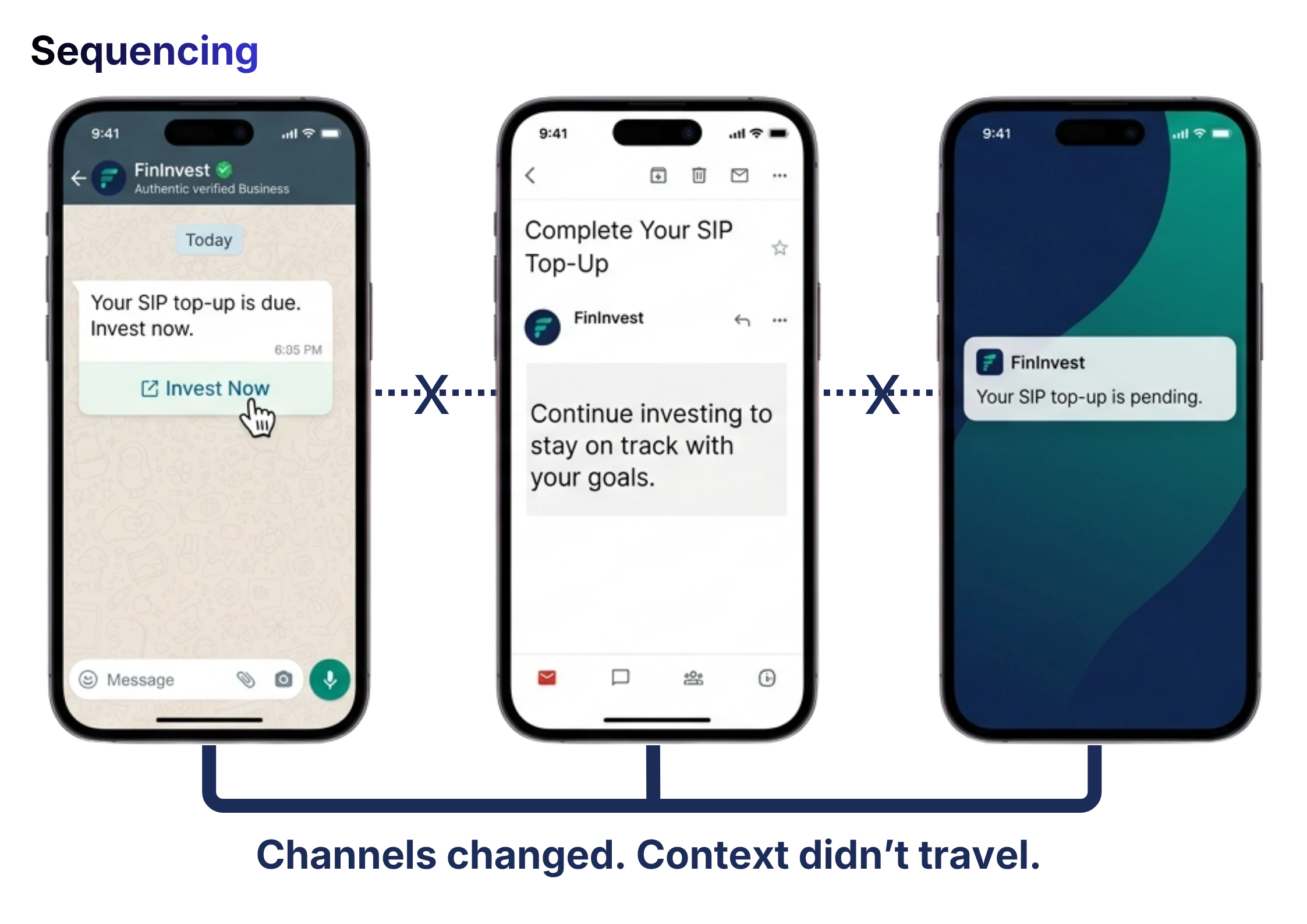

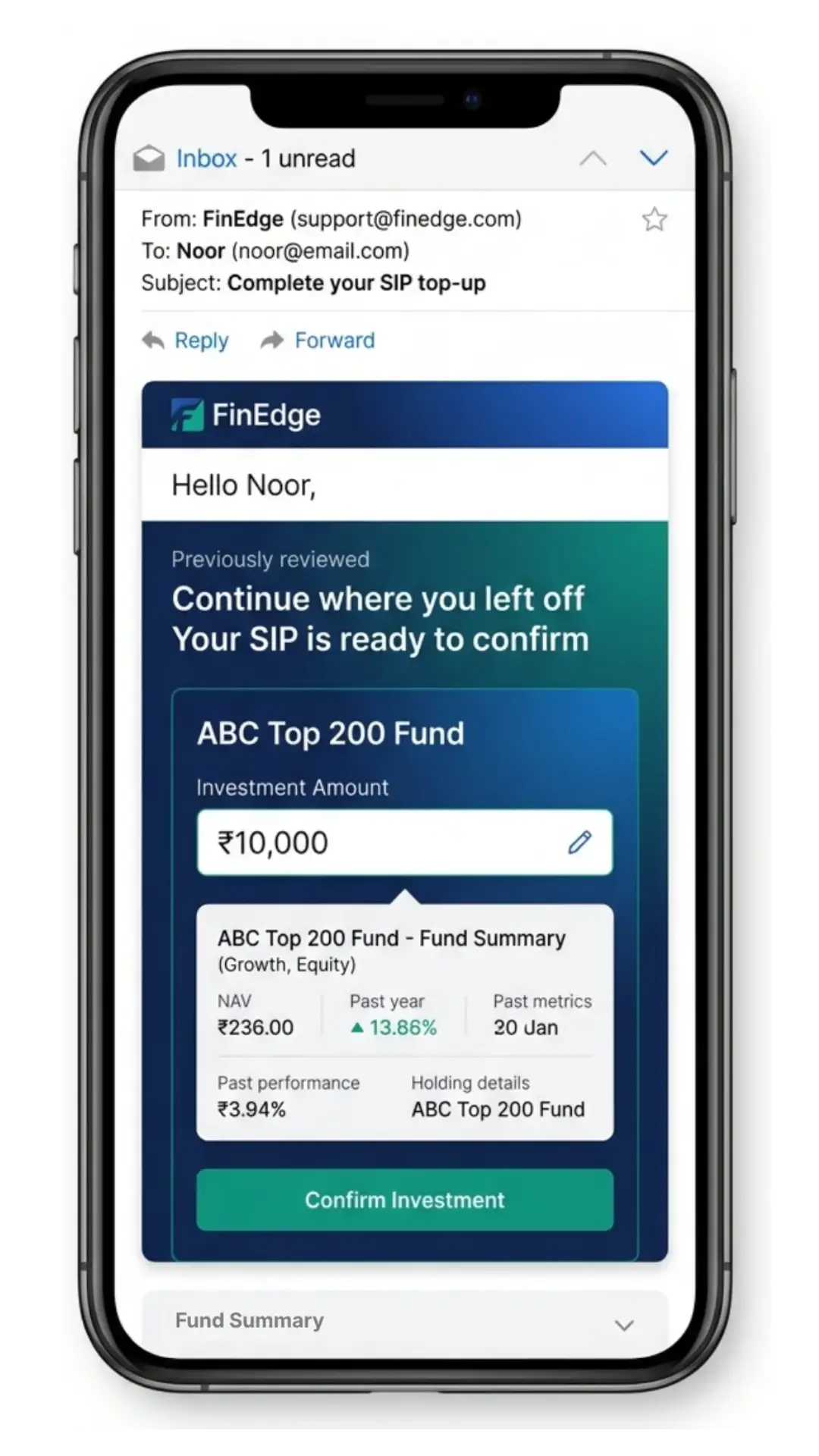

- An SIP top-up reminder reaches an investor by email, and the fund house portal it opens has no memory of the nudge, the amount, or the fund; the investor starts from scratch.

The trap isn’t set when the campaign fails to reach the customer. It’s set when the journey loses them between channels.

What It Is Actually Costing

The commercial case for closing the handoff trap is a unit economics argument, and it sharpens considerably when rising acquisition costs sit next to the revenue that broken customer journeys leave on the table.

Digital acquisition costs across India’s BFSI sector have risen 20-30% annually as paid channels become increasingly contested. Across Southeast Asia, where digital banking and insurance penetration is still expanding, the acquisition curve is steeper still.

When a customer’s journey breaks mid-transfer, and they disengage, that acquisition spend does not disappear; it waits. The brand will run a retargeting sequence, a re-engagement push, each carrying its own cost and its own probability of finding the customer in the same receptive moment. Most of the time, the moment has passed. Intent is not durable. What follows is not recovery but re-acquisition.

The trap also shows up differently depending on where you sit in BFSI, but it shows up everywhere. There is a regulatory dimension to this cost too, one that rarely makes it into marketing conversations but sits clearly in the CFO’s line of sight. India’s Digital Personal Data Protection Act and equivalent frameworks across Southeast Asia, such as Singapore’s PDPA, Indonesia’s OJK, and Malaysia’s BNM, mean that re-engaging a dropped customer is not just a media spend decision. It is a fresh consent, a new audit trail, and additional compliance overhead every time the cycle restarts. The cost of a broken journey is not just what you spend to reach the customer again. It is what you spend to make that re-engagement compliant.

The revenue picture on the other side of this is equally clear.

McKinsey’s research on omnichannel banking shows that reducing friction and carrying customer context across channels can improve sales productivity by as much as 40%. Real omnichannel strategies raise revenue by 10-15% and improve customer satisfaction by 20-30%. Additionally, customers who receive high-quality omnichannel experiences are 3.6x more likely to purchase additional products.

The inverse of all three, what brands are actively losing by not closing the journey continuity gap, is the true cost of the handoff trap.

What Closing It Actually Requires

Naming the trap is the first step. The second is understanding that closing it is not a channel decision but an orchestration one.

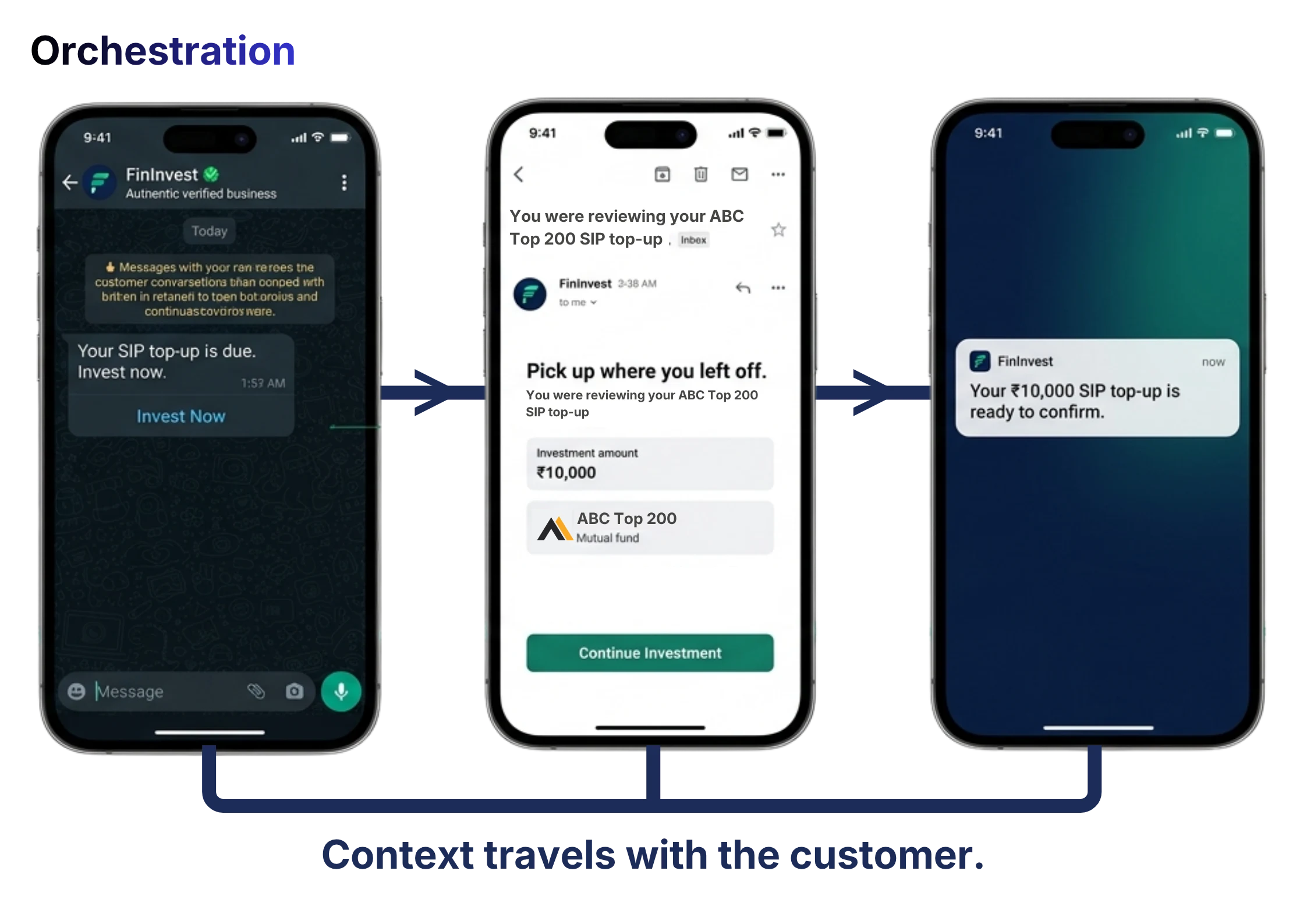

Most BFSI brands approach omnichannel engagement as a sequencing problem: send on WhatsApp first, follow up on Email, retarget on the app. But sequencing is not orchestration. Sequencing puts the customer through a predetermined order of channels. Orchestration carries the customer’s intent, context, and journey state across every channel in real time, so that when a policyholder clicks a renewal reminder on WhatsApp but doesn’t complete, the email that follows doesn’t start the conversation over. It picks it up exactly where the handoff broke.

That distinction between sequencing and orchestration is where most omnichannel stacks fall short. The channels are connected at the campaign level but disconnected at the journey level. Customer context doesn’t travel. Completion state isn’t shared. Each channel treats the customer as if they arrived fresh, because to that channel’s underlying system, they did.

Closing the handoff trap requires a customer engagement platform that unifies journey logic across WhatsApp, Email, Apps, and emerging channels, not just coordinating when messages go out, but carrying what the customer did, what they didn’t complete, and what the next best action is, regardless of which channel surfaces it. The transaction completes on whichever channel the customer is most ready to finish on, not on whichever channel the campaign was originally designed around.

Orchestration in Practice

The difference between sequencing and orchestration becomes visible the moment you see it working. Across a unified customer engagement platform, it shows up in many ways; here are a few of them:

Intelligent Nudges

Triggered not by a campaign calendar but by what the customer did or didn’t do. A customer who opened a loan offer on WhatsApp but didn’t complete gets a nudge on their next most active channel; the journey picked up exactly where it broke, with full context of how far they got.

AMP Interactive Emails

The inbox becomes an action surface, not a redirect. A customer can review a fund or confirm a renewal without leaving their email. And if they still don’t complete, the platform carries that signal forward, so the WhatsApp follow-up that arrives next already knows what they saw, what they didn’t act on, and what to say differently.

End-to-End WhatsApp Journeys

From the first message to the final confirmation – policy issuance, loan disbursement, or payment receipt, entirely within the same thread. No switch, no session expiry. For journeys where WhatsApp is where the customer lives, the platform lets the entire transaction live there too.

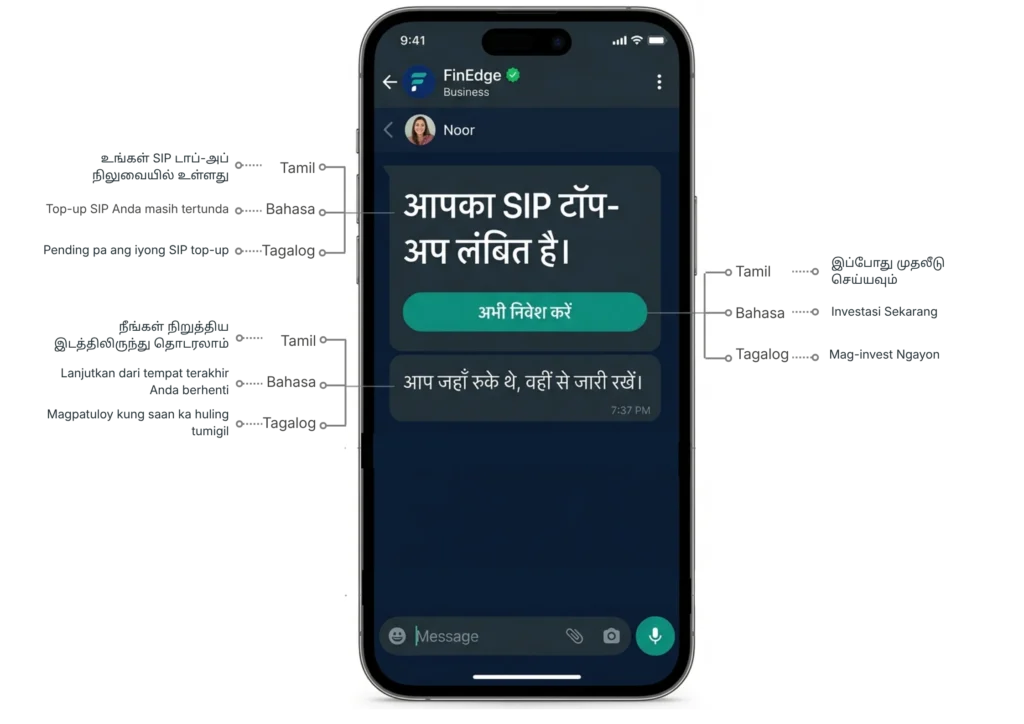

Vernacular at Scale

A customer who begins their journey in Hindi on WhatsApp shouldn’t have to continue it in English on Email or the app. Orchestration that carries language preference across every channel touchpoint – Hindi, Tamil, Bahasa, or Tagalog ensures the context that travels isn’t just transactional. It’s human.

The Question for the Next Quarterly Review

There is a question most BFSI marketing teams have never formally asked, not because it is complicated, but because the answer requires looking across silos that rarely talk to each other.

When a customer’s journey starts on WhatsApp and doesn’t complete, does our Email know? Does our app know? And does our customer engagement platform carry that context forward, or does it start the conversation over?

For most BFSI brands, the honest answer is the latter. The channels are live. The campaigns are coordinated. But the journey intelligence that should sit underneath, the layer that knows what the customer attempted, where they dropped, and what the next best action is, regardless of channel, is either absent or fragmented across vendors who don’t share data in real time.

Every brand reading this has an omnichannel presence, but the orchestration is its real problem. And it is the reason clicks keep outpacing conversions, no matter how well the campaign performs.

The brands that close this gap in 2026 will not be the ones that add another channel to their mix. They will be the ones whose customer engagement platform treats every channel not as a separate campaign surface, but as one continuous journey, where context travels with the customer, and completion is the metric that matters. The handoff is never the end of the road.

Shriram Finance closed the handoff gap using Netcore’s CE platform, achieving an 81X ROI and a 40% Lift in Engagement.

Read the full story here.

Explore how financial services brands are rebuilding their customer engagement architecture to close the handoff trap.