TL;DR

- Agentic AI helps banks move from reactive customer engagement to real-time, autonomous decision-making.

- Banks are using agentic AI for personalized onboarding, user retention, customer support, and proactive engagement.

- Unlike traditional automation, agentic AI in marketing continuously learns from customer behavior and adapts dynamically.

- The biggest impact areas include improved trust, higher retention, faster service resolution, and better customer lifetime value.

- The future of banking will be driven by intelligent, personalized, and always-on customer experiences powered by AI.

Silent funnel leakage across digital applications is the greatest unmeasured loss in modern retail banking. While the industry has spent years obsessively optimizing reactive chatbots, we missed the fundamental architectural shift from basic generative responses to fully autonomous, intent-driven workflows. Agentic AI in marketing is the bridge that closes this gap, turning disconnected data silos into unified, hyper-personalized retention engines that operate with complete accountability for outcomes.

What is Agentic AI in Banking?

Agentic AI in banking is an autonomous system that uses artificial intelligence to pursue specific financial or operational goals without requiring step-by-step human prompts. Unlike traditional chatbots that only answer questions, AI agents can independently reason, remember past interactions, access banking tools, and proactively execute complex workflows to drive measurable customer retention.

Let’s start with what intent-driven autonomy actually means in a financial context. For the last two years, banking leaders have experimented heavily with generative AI. You have likely tested Large Language Models (LLMs) to draft emails, summarize regulatory documents, or power customer service bots. But generative AI, by its nature, is passive. It sits and waits for a user or an employee to give it a prompt.

Agentic AI in marketing flips that dynamic entirely. We are moving from “assist me” to “do it for me within defined guardrails.

An AI agent is given a macro-level objective such as “reduce abandonment in the personal loan KYC process by 10%” and it possesses the systemic autonomy to decide how to achieve that goal. As noted by McKinsey, “Agentic AI is rapidly emerging as a game changer for banks, shifting operations from reactive to proactive.”

At Netcore, we view this shift as the ultimate expression of intelligence over execution. We believe that technology should be accountable for real business results, not just software capabilities.

How does Agentic AI Differ from Conventional Banking AI Tools?

To fully grasp the magnitude of this market reality, you must understand how agentic systems break the limitations of the marketing automation software you currently use. Traditional banking tools rely on rigid “if-then” rules. If a customer abandons a fixed deposit application, wait 24 hours, then send an email.

This rules-based approach creates terrible customer experiences because it lacks context. If a user abandoned the application due to a technical server error, sending them a promotional email 24 hours later destroys trust. An agentic system, on the other hand, reasons through the context. It sees the server error, pauses the promotional campaign, and immediately deploys an in-app nudge offering technical support.

What are the Core Applications of Agentic AI in Modern Banking?

When we deploy our agentic marketing platform for retail banks and Non-Banking Financial Companies (NBFCs), we do not focus on hypothetical efficiency gains. We focus on fixing broken funnels.

Here is how agentic AI in marketing is currently being applied to solve the most expensive problems in digital banking:

1. Autonomous Funnel Recovery and Orchestration

In retail banking, applications for Personal Loans, Two-Wheeler Loans, and Fixed Deposits often involve complex, multi-step digital paths: OTP verification, PAN card submission, KYC processing, and deposit verification. Traditionally, nearly 95% of potential conversions are lost before the final payment because there is limited visibility into where users abandon the process. Agentic AI continuously monitors these funnels, identifies the exact moment of drop-off, reasons why the user left, and autonomously orchestrates real-time, highly contextual personalization interventions across web, app, and email to bring them back.

2. Dynamic Cross-Selling Through Behavioral Nudges

Agentic AI in marketing doesn’t just recover lost leads; it actively creates new revenue by understanding predictive intent. For example, when we partnered with Bajaj Markets, a digital-first marketplace offering loans and investments, they needed to optimize campaign performance without increasing budgets. By integrating our Agentic Marketing capabilities to generate optimized, AI-driven App Push variations tailored to user behavior, they achieved a 17% Month-over-Month growth in App Lead Conversions and a 360% increase in overall conversions. Read the full success story.

3. Interactive Financial Education and Gamification

Customer retention requires engagement outside of active transaction windows. Navia Markets leveraged our Product Experience platform to deploy interactive gamification and contextual video nudges during non-trading days. By treating education as an autonomous, hyper-personalized journey, they achieved a 48% uplift in app sessions and doubled their average session time, proving that well-timed intelligence dramatically boosts engagement. Read the full success story.

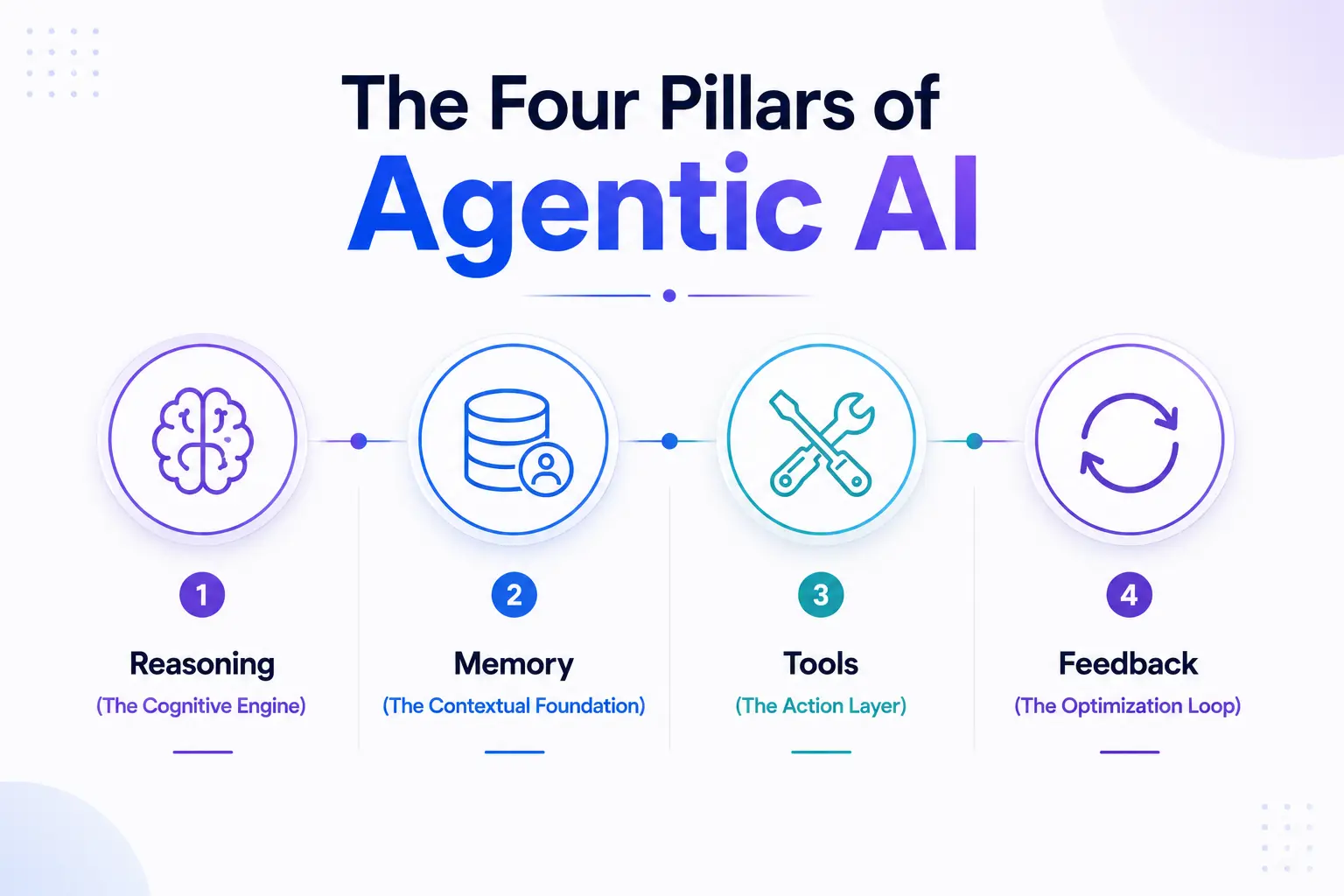

The Four Pillars of Agentic AI in Marketing

To demystify how these systems actually function, we must look at their underlying architecture. According to Deloitte, “AI agents can independently reason, execute complex tasks, and achieve targeted goals safely within banking frameworks.” This capability is constructed on four foundational pillars.

1. Reasoning (The Cognitive Engine)

Unlike a standard algorithm that executes a hardcoded rule, an agentic system breaks down complex goals into smaller, logical steps. If the goal is “Increase Fixed Deposit completion rates,” the agent reasons: *I need to identify where users are dropping off. I see a spike in drop-offs at the PAN card upload. I should create an intervention specifically for that step.*

2. Memory (The Contextual Foundation)

Agents possess both short-term memory (what the user clicked on three seconds ago) and long-term memory (the user’s loan history over the last five years). This persistent memory ensures that the agent never treats an existing, high-value customer like an anonymous website visitor. It unifies the view across web, app, and call center data.

3. Tools (The Action Layer)

An agent is useless if it cannot take action. Agentic AI in marketing is deeply integrated into your tech stack. It has “tools” it can use, it can query the CRM, trigger an email via the Customer Engagement Platform (CEP), push a dynamic personalized banner to the website (PZ), or send a WhatsApp message. It autonomously selects the right tool or calls an agent for the job based on the user’s historical channel preference.

4. Feedback (The Optimization Loop)

Agentic systems continuously learn. If the agent deploys an educational nudge to users stuck in the KYC flow, it monitors the conversion rate. If the nudge performs well on mobile but poorly on desktop, the agent ingests that feedback and autonomously adjusts its deployment strategy in real-time, optimizing without human intervention.

Case Study: How Shriram Finance achieved 171X ROI with Agentic Marketing

Theory is helpful, but banking leaders demand undeniable proof. We speak in results and specifics, not vague promises.

Shriram Finance is India’s largest retail NBFC, managing ₹2.72 lakh crore in Assets Under Management (AUM) across 9.7 million customers. Despite this massive scale, they discovered silent revenue leaks across their digital funnels for Fixed Deposits, Personal Loans, and Two-Wheeler Loans.

The Problem: They had no central system to manage drop-offs. If a user dropped off the website, that data wasn’t immediately linked to their call center interactions. Nearly 95% of potential conversions were lost before payment. Furthermore, their existing re-engagement was generic. A user who dropped off due to a technical error in KYC was treated exactly the same as a user who abandoned the final payment stage.

The Solution: Shriram Finance implemented Netcore’s full-stack Agentic Marketing solution, unifying our Customer Engagement Platform (CEP), Product Experience (PX), and Personalization (PZ) suites.

Instead of generic follow-ups, our agentic system created funnel-driven journeys tailored to specific drop-off zones. It deployed real-time interactive app nudges and contextual web messages to engage high-intent visitors immediately. Furthermore, it integrated missed call data to create an automated nurture journey for leads generated after hours.

Check out Shriram Finance’s Success Story

The Measurable Outcomes:

- 171X Return on Investment (ROI): Driven by entirely optimized funnel efficiency.

- 130X Growth in Revenue: A massive leap from 81X just 6 months prior, directly attributed to improved lead capture.

- 12% Improvement in Lead Capture: By closing the call center leakage gap and automating after-hours engagement.

- 22% Drop in Cost of Acquisition (COA): Greater operational efficiency meant less spend was required to acquire a paying customer.

As Manoj Nair, SVP of Digital Transformation at Shriram Finance, stated: “The integration of website journeys, call-centre flows, and data-driven segmentation has enabled us to capture leads more effectively and enrich them with the right insights. This has not only reduced leakages in our funnels but has also improved conversion efficiency.”

Final Take

Agentic AI is redefining how banks build trust, engagement, and long-term customer relationships. Instead of relying on static automation and reactive communication, banks can now use AI to anticipate customer needs, personalize interactions in real time, and proactively reduce churn.

As customer expectations continue to rise, the future of banking will belong to institutions that combine intelligence, personalization, and autonomous decision-making to deliver seamless, trusted experiences at scale. Interested to work alongside someone who has done this already before? Talk to us. We have helped numerous banking organizations and leading players globally.