A 2026 reading on the hidden cost of broken journeys across financial services in India and Southeast Asia

In 2026, the average BFSI customer journey looks complete on paper. A policyholder receives a renewal nudge on WhatsApp. A fintech user sees a pre-approved loan offer inside an app. An AMC investor receives a SIP top-up reminder by email. Each of these is a customer at the moment of highest intent, the moment closest to revenue. And yet, across most BFSI brands in India and Southeast Asia, that moment is also when the journey breaks.

The customer is asked to switch channels. Reload a browser. Open another app. Authenticate again. Fill in the same details a second time. By the time they arrive at the transaction screen, a measurable share of them are gone.

That gap between intent and transaction has a cost. We will call it the redirect tax. It is the amount BFSI brands pay, every quarter, to reacquire customers they have already won.

The redirect tax, defined

The redirect tax is paid every time a journey is forced to switch channels mid-transaction. What matters is not where the customer started or where they were pushed. It is that the journey broke before the transaction completed, and each break is a chance to lose a customer the brand has already paid to acquire.

The number across BFSI is not small. 67-70% of banking customers abandon onboarding when it exceeds 10 minutes due to poorly sequenced KYC and onboarding. In digital lending, if an account opening or loan application takes longer than five minutes, abandonment rises to 60% or more.

Insurance is no different. In India, where over 90% of retail policies were issued digitally in 2025, the renewal stage tells a quieter story. Roughly 40% of Indian policyholders do not renew their insurance annually, and the primary causes are not price. Forgetfulness accounts for 45% of lapses, perceived complexity for 30%, and lack of engagement for 25%. All three are journey problems, not product problems.

For AMCs, the equivalent break is the SIP start. KYC, mandate setup, fund selection, payment authorisation. Each step traditionally lives on a different surface. Every additional surface adds drop-off.

For NBFCs and digital lenders, the same logic plays out in the loan application flow. Indonesia’s OJK data shows P2P loan books at IDR 80.94 trillion as of April 2025, up 29% year on year, and yet the share of applications that complete on the first attempt remains a stubborn industry concern.

| Wherever the redirect happens, the result is the same. The brand has paid once to bring the customer to the moment of intent. When the journey breaks, the brand will pay again to bring them back. That is the tax. |

Why is this a 2026 problem?

The redirect tax has always existed. What has changed is the cost of paying it. Three forces have pushed it from a tolerable inefficiency into a P&L item that no CMO can leave unmanaged.

The first is regulation. India’s Digital Personal Data Protection (DPDP) Act, in force through 2025, has raised the compliance cost of every consent collected outside a verified, logged channel. Indonesia’s OJK, Singapore’s PDPA, Malaysia’s BNM, and the Philippines’ BSP have all moved in the same direction. Reacquiring a customer who dropped off no longer costs only media spend. It costs another round of consent, another exposure window, and another compliance overhead that the CFO can see on the quarterly review.

The second is rising CAC. Digital acquisition costs in BFSI rose throughout 2025, even as branch acquisition remained flat. The penalty for losing a digitally acquired customer is higher now than it has ever been.

The third is technology. The channels that made redirects necessary five years ago can now hold the entire transaction. The conditions that made the tax acceptable have closed. The conditions that make it eliminable are open. The math has changed underneath the brand, even when the journey design has not.

What it takes for a channel to actually close a transaction

The reason most BFSI brands continue to pay the tax is simple. They have built their customer engagement strategy around channels that move information, not channels that complete transactions. Those are different problems.

For a channel to close a financial transaction natively, three conditions have to sit on the same surface:

- Authenticated identity

- A native payment rail

- In-channel journey orchestration.

If any one of these is missing, the customer has to switch to finish, and the redirect tax gets paid.

This is where 2026 looks different. The conditions have started to converge on more than one channel. A well-designed banking app holds all three when the customer’s intent originated in-app: a balance check, a fixed deposit booking, and an in-session top-up. Email is approaching the same capability for journeys where authentication and AMP-driven interactivity keep the transaction inside the inbox. In many customer journeys today, WhatsApp is no longer supporting the app experience; it is rather becoming the primary interface customers return to more often than the app itself. And WhatsApp, in particular, has crossed into transaction territory faster than most CE strategies have caught up with.

BFSI is now the largest end-user vertical for WhatsApp Business API globally, with the segment projected to grow at an 18.1% CAGR through 2034. UPI on WhatsApp is now open to all Indian users after NPCI removed onboarding caps, and equivalent rail integrations are maturing across QRIS in Indonesia, PayNow in Singapore, DuitNow in Malaysia, and GCash and InstaPay in the Philippines. The point is not that one channel has won. The point is that for the first time, several channels are capable of completion, and the brand’s job is to make the transaction finish where the intent was born.

The Real Failure Point in Most WhatsApp Journeys

There is one operational tax inside the redirect tax that most BFSI marketing teams have felt firsthand. The engagement platform builds the campaign. A separate CPaaS vendor handles the WhatsApp send. Templates get manually replicated across systems. Then, mid-cycle, a utility template gets reclassified as marketing. The per-message rate jumps, the team goes back to re-templatization, and days fall off the campaign timeline. For a mid-to-large BFSI brand running hundreds of WhatsApp campaigns a year, that is a recurring drain on budget, bandwidth, and live campaign integrity.

This is where premium Meta partner status matters in practice. Netcore extends the capability to automatically disable template delivery when a category mismatch is detected, reducing the risk of continued sends under the wrong classification. While category changes can still occur, tighter platform-level detection and routing reduce manual intervention, contain downstream impact faster, and help marketing teams keep campaigns aligned to the timelines they originally planned.

What the one-stop policy shop actually looks like

Consider four journeys across Banking, Insurance, and AMC, each beginning on a different channel, each completing without a redirect.

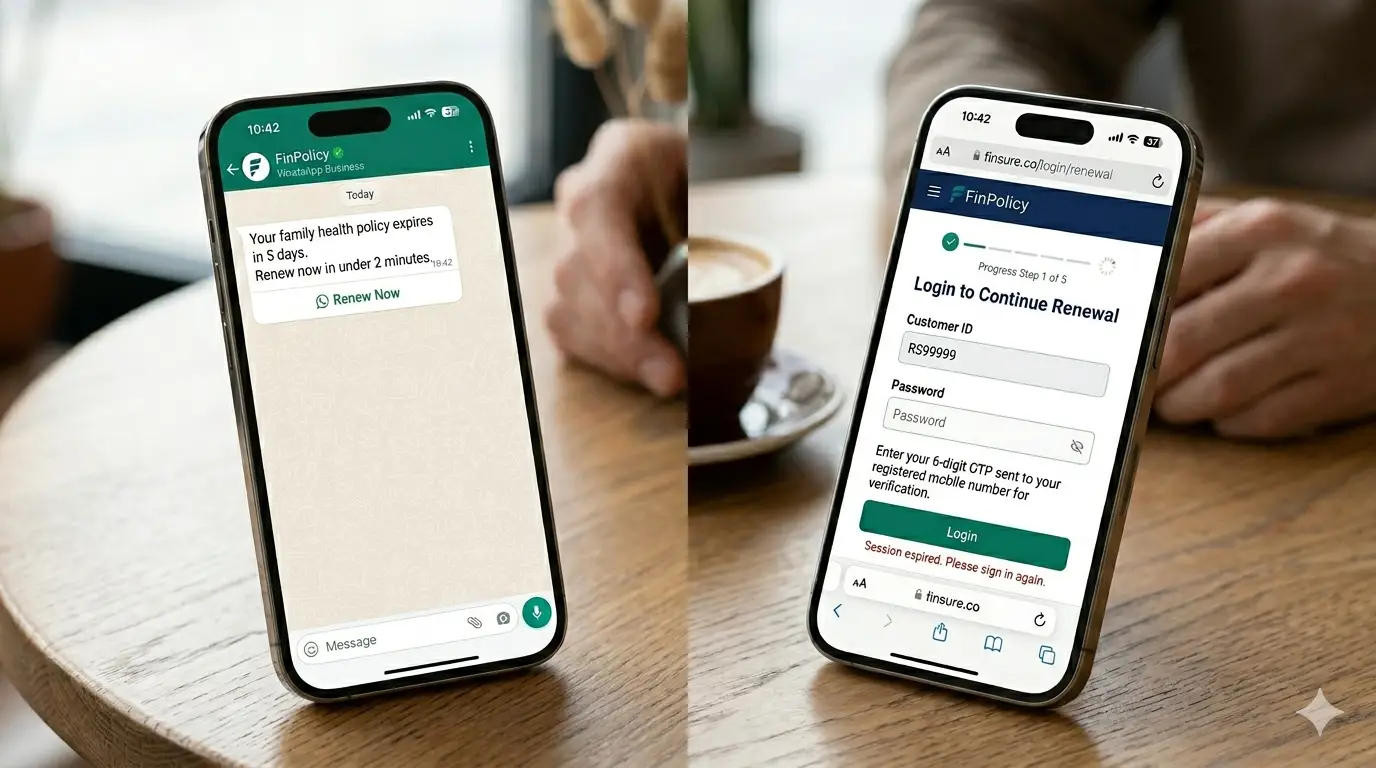

- Renewal on WhatsApp

An insurance renewal reminder reaches the customer on WhatsApp. The premium is shown inside the thread. The policy details open in the chat. The customer verifies their information, pays through UPI inside the chat, and receives the renewed policy in the same thread. No app open required.

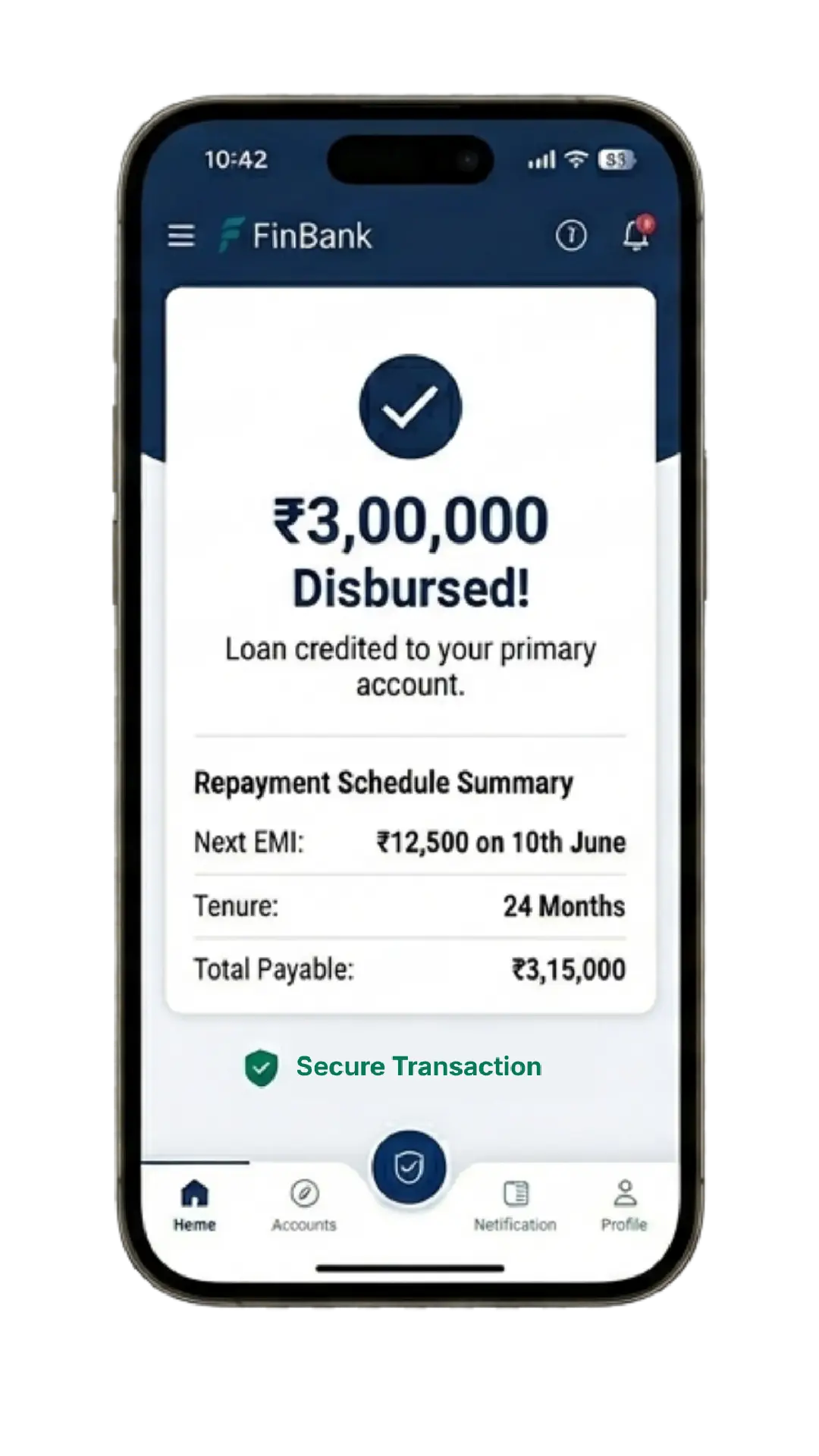

- Instant loan inside the app

A pre-approved personal loan offer pops up in a bank app after a balance check. Document re-use pulls existing KYC from the customer’s profile. The customer reviews and signs the application on the same screen, and the loan is disbursed instantly. No browser tab opens.

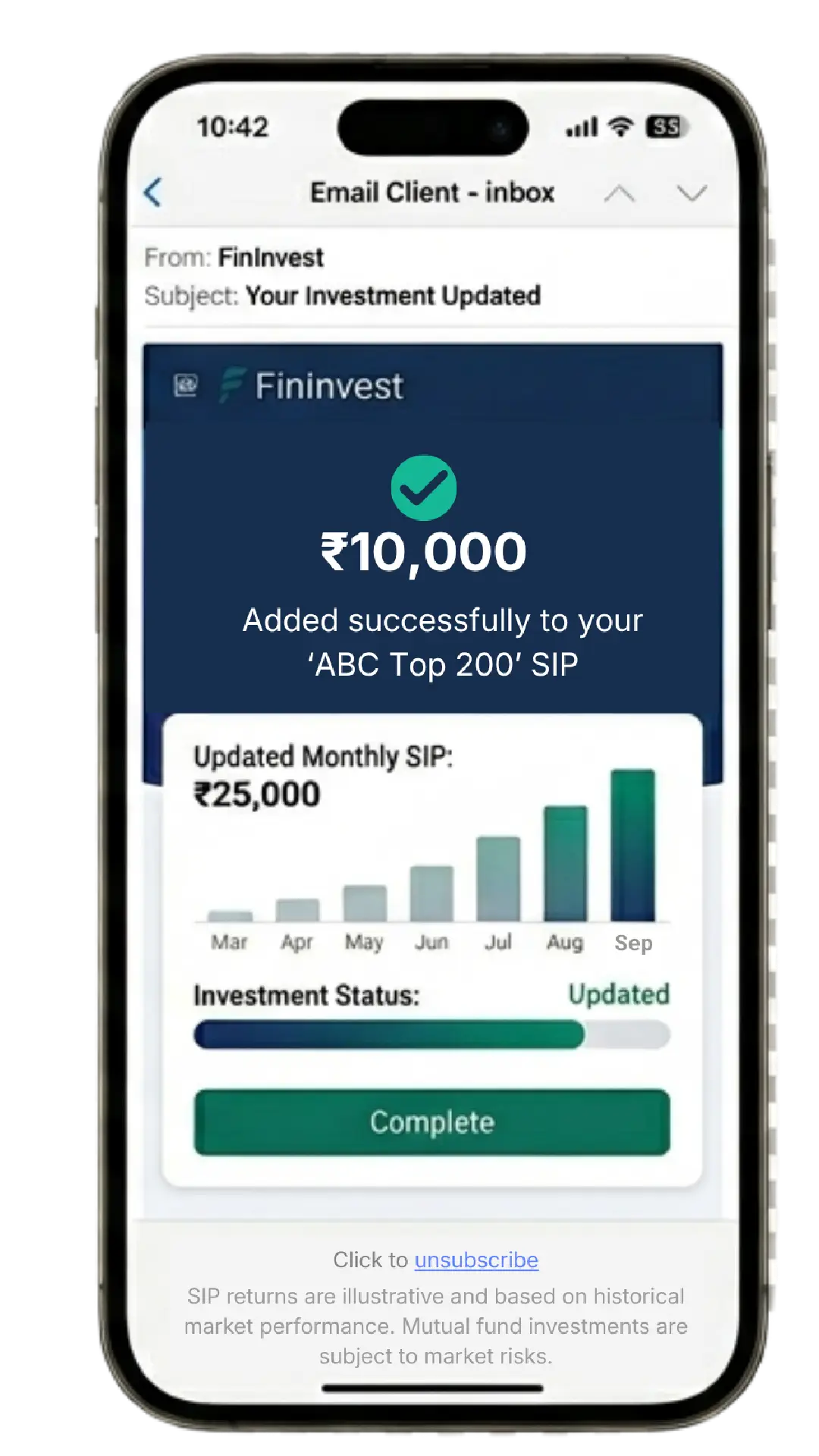

- SIP top-up in the inbox

An AMC sends an interactive, in-inbox (AMP) email to an existing investor. Fund selection happens inside the email itself, without leaving the inbox.

- Motor cover from a click-to-WhatsApp ad

A motor insurance journey begins on a paid ad that opens a WhatsApp chat. Vehicle details, NCB capture, premium comparison, payment, and policy issuance all sit inside the same conversation.

Each of these journeys requires a customer engagement platform that is deep enough on the originating channel to hold the entire transaction, and intelligent enough across channels to route the journey to where it will most cleanly close. Without a unified customer engagement platform underneath, even capable channels operate in silos, making it impossible to preserve customer context, coordinate journeys in real time, or consistently close transactions where intent actually forms. That is the difference between a message platform and a completion platform.

The CMO question for 2026

| On each channel where my customers form intent, can the transaction complete inside that channel, and is my customer engagement platform deep enough on every one of those channels to make that true? |

This is the question every BFSI CMO should be asking in the next quarterly review. It is a sharper question than “do we send on WhatsApp.” It is a more useful question than “what is our channel mix.” It cuts directly to the redirect tax, and it produces a buying criterion that the rest of the leadership team can hold onto.

The CFO will read it as a cost question. The CDO will read it as an architecture question. The CIO will read it as a vendor question. The CMO is the only person in the room who reads it as all three at once. Which is why the answer cannot be delegated.

Closing the gap

The redirect tax is paid in the gap between intent and transaction. Every channel switch widens the gap. Every native completion closes it. The brands that recover the fastest in 2026 will be the ones whose customer engagement platform can hold the whole journey on whichever channel the customer started on, and switch to another only when the customer’s intent moves first.

In a 2-minute walkthrough, see a full BFSI transaction journey finish inside a single WhatsApp thread, from intent to conversion. The same orchestration runs across your app, your email, and your web journeys. WhatsApp is just the channel where the gap is widest in 2026, and the one where closing it pays back the fastest.